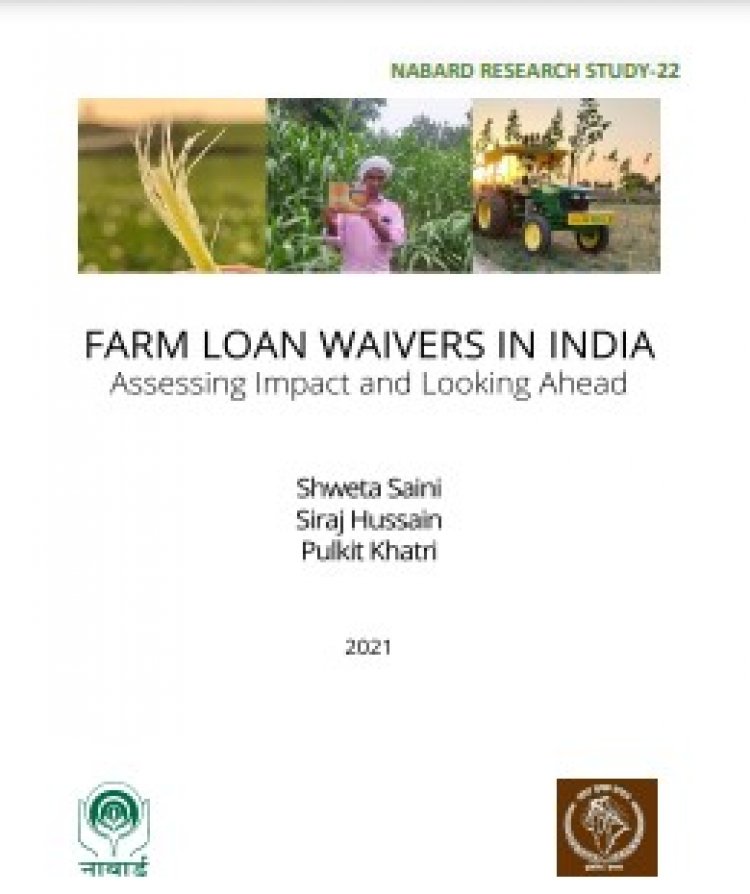

Farm loan waivers do not improve condition of farmers; they increase chances of wilful default: BKS-Nabard report

The condition of the farmers does not improve as a result of farm loan waivers (FLWs). It takes only a few years for the farmers to become indebted again before they need another round of waivers soon. This is the finding of a study funded by Nabard’s Department of Economic Analysis and Research (DEAR) and facilitated by Bharat Krishak Samaj (BKS). The BKS–Nabard report says that FLWs only increase the chances of wilful defaults by farmers. It pushes honest farmers to default on agricultural loans.

Join the RuralVoice whatsapp group

Join the RuralVoice whatsapp group

The condition of the farmers does not improve as a result of farm loan waivers (FLWs). It takes only a few years for the farmers to become indebted again before they need another round of waivers soon. This is the finding of a study funded by Nabard’s Department of Economic Analysis and Research (DEAR) and facilitated by Bharat Krishak Samaj (BKS).

The BKS–Nabard report says that FLWs only increase the chances of wilful defaults by farmers. It pushes honest farmers to default on agricultural loans. The farmer behaviour and attitudes towards these waivers were studied through a primary survey of about 3000 farmers from three states of Punjab, Uttar Pradesh (UP) and Maharashtra.

To support a distressed farmer in a sustainable manner that empowers him/her in both the short and long run, therefore, requires a rethink, says the report. It makes a case for a deeper analysis of the structural factors that consistently cause distress to the farmers.

Farmers borrow more from institutional sources

According to the report, about 89.3 per cent of the farmers in Punjab, 79.2 per cent in Maharashtra and 74.8 per cent in UP borrowed from institutional sources like banks. There is a huge difference between the interest rate on institutional loans and that on non-institutional loans. The interest rates paid by the farmers on non-institutional loans were found to range between 9.5 and 21 per cent. Those on institutional loans ranged between 5.9 per cent and 7.7 per cent.

In terms of the proportion of loan amounts, about 75 per cent in Punjab, 83 per cent in Maharashtra and 76 per cent in Uttar Pradesh were taken from institutional sources. An average Punjab farmer was found to be borrowing a much larger amount. On average, a marginal farmer in Punjab annually borrowed about Rs 3.4 lakh. This amount in UP and Maharashtra was about Rs 84,000 and Rs 62,000 respectively.

There is a diversion of agricultural loans towards non-agricultural use. The diversion of Kisan Credit Card (KCC) funds appears to be the highest in the case of Punjab and the lowest in the case of UP. It was also found that for an average farmer diversion of funds is inevitable and critical for survival.

Factors causing distress to farmers

There are several reasons for the farmers’ distress in the states of Punjab, UP and Maharashtra. Income instability due to increased cost of cultivation, damage to crop/livestock or fall in market prices received by farmers emerged as primary reasons in the study. Besides, climate- and weather-related issues caused much distress to the farmers. Farmers in the three states did not rank indebtedness as any different than how they ranked other factors causing them distress.

Issues with infrastructure mainly on account of erratic power supply were cited as one of the many distress factors for which no farmer in the three states seem to have any coping mechanism. Problems of marketing included non-transparency in market transactions and excessive dependence on middlemen. To counter market-related distress, farmers are accessing self-help groups (SHGs) and farmer producer organizations (FPOs) in Maharashtra and UP. Increased labour costs and lower quality inputs resulting in decreased quality of farm produce pushed up the costs of cultivation.

The absence of crop insurance or delay in receiving compensation was cited as an important cause of distress in all three states. While some reduced personal expenditure to overcome the distress, others increased their non-institutional borrowings. To counter the rising cost of capital, farmers prefer to rent agricultural equipment and machinery rather than own it, particularly in UP and Maharashtra.

“Very highly” distressed surveyed farmers did not receive any FLW benefits

The study has come up with some other findings. An increase in the proportion of irrigated land is associated with lower farmer distress. A larger household size is associated with lower farmer distress. Farmers with diversified sources of loans were less distressed. Higher amounts of loans taken from non-institutional sources were associated with higher distress. Being an FLW beneficiary did not have a statistically significant impact on decreasing farmers’ distress levels.

According to the report, in all three states together, more than 40 per cent of the “very highly” distressed surveyed farmers did not receive any FLW benefits. In fact, FLW only benefited a small group of the actual distressed farmer population. There was marginal or no problem in accessing fresh credit for an FLW beneficiary in all the three states. Perhaps this is why FLW increased the chances of wilful defaults by farmers. 68-80 per cent of the respondents in the three states agreed to this increase in chances. 72-85 per cent of respondents in the three states agreed FLW pushed honest farmers to default on agricultural loans. The possibility of default was higher on institutional loans than on non-institutional loans.

Conclusion

Ajay Vir Jakhar, Chairman, BKS, says that the report “correctly summarizes that in the circumstances, indebtedness in Indian agriculture is inevitable and indebtedness is more of a symptom of farmer distress than its immediate cause.”

He adds, “The major problem of farm loan waivers arises from the design of the waiver itself. A large section of the people whose loans should have been waived were unable to benefit from the process. BKS believes using the Gram Sabha to identify the really deprived and distressed would be the right way.”